Yield Stablecoins: A New Frontier of Banking Risk

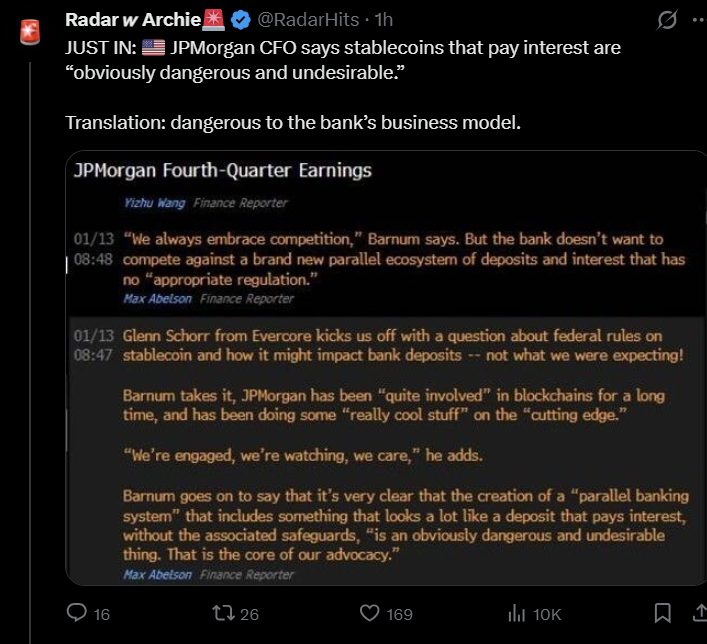

The debate surrounding stablecoins has intensified, with JPMorgan, through its CFO, raising concerns about the risks associated with yield stablecoins. The banking institution is advocating for strict regulation via the GENIUS Act to prevent a drift toward a form of unregulated parallel banking.

Just a few days after JPMorgan was downplaying fears related to stablecoins, these assets that have become essential in the crypto world, a new generation of yield stablecoins is causing worry among traditional banks. These new stablecoins promise interest to holders, mimicking interest-bearing bank deposits but without adhering to regulatory rules. JPMorgan views this development as a direct threat to the regulated banking system.

JPMorgan's CFO, Jeremy Barnum, has emphasized that these products are creating a form of parallel banking, bypassing the safeguards imposed on financial institutions. The risk is twofold: a potential loss of deposits for banks and a weakening of systemic control.

By draining liquidity out of the banking circuit, these stablecoins could potentially destabilize the financial balance. The concern expressed by JPMorgan highlights the growing tension between crypto innovation and economic stability, underscoring the need for urgent regulation.

The GENIUS Act: An Attempt at Targeted Regulation

In response to JPMorgan’s concerns, the GENIUS Act has emerged as a legislative solution. This bill aims to regulate stablecoins and establish clear rules for their issuance and use. Recent amendments specifically target yield stablecoins, proposing to forbid interest payments solely for holding a token. The objective is to limit abuses and prevent these assets from becoming direct substitutes for bank deposits.

The GENIUS Act seeks to strike a balance between innovation and security, allowing stablecoins to develop while ensuring consumer protection and the stability of the financial system. For players in the crypto space, this regulation presents a significant challenge: adapting their business models and anticipating legal constraints. The future of stablecoins will ultimately depend on their ability to integrate within this regulatory framework.

Towards a Confrontation Between Decentralized Finance and Banking Institutions

JPMorgan’s call for the regulation of stablecoins signifies a strategic confrontation between two distinct worlds. On one side is decentralized finance, striving to offer alternatives to traditional banking services. On the other are financial institutions, determined to maintain their central role in the economy. Yield stablecoins serve as a focal point for this opposition, as they directly threaten the classical banking model.

For crypto projects, the challenge lies in discovering solutions that are compatible with regulation, potentially utilizing mechanisms such as staking, as seen with Ethereum, or through governance models. For banks, the imperative is to defend their position and avert massive disintermediation. This inherent tension could escalate into an open conflict, with each side deploying its economic and political arguments.

The evolution of the GENIUS Act will be a critical factor in determining whether a compromise is achievable or if the conflict will intensify.

JPMorgan’s warning regarding yield stablecoins aligns with the three major flaws in stablecoins identified by Vitalik Buterin, further emphasizing the crucial importance of this issue for the future of crypto. The GENIUS Act could potentially become the reference framework for regulating these assets. However, the fundamental question remains open: will regulation stifle innovation, or will it foster a sustainable coexistence between banks and stablecoins?