Why “Brand Stables” Matter More Than You Think

First, let’s talk about brand stablecoin tokens issued by companies that already have a massive user base and significant trust equity.

The logic is simple: if a dollar‑pegged token can be dropped into an existing app wallet millions of users already open daily, it jumps friction ahead of any “crypto native” alternative.

A token backed by a known name carries built‑in credibility, regulatory visibility, and easier adoption in merchant ecosystems.

These brand stables don’t just help with trust; they monetize cleverly too. Because many users hold balances, issuers can invest reserves in short‑term, high‑quality assets and capture yield (“float income”).

Add in cross‑border fees, merchant integrations, and treasury services, and you get a revenue engine layered on top of the token’s utility.

Fintech L1s: Building the Rails from Scratch

Owning the token is one thing. Owning the rails is another. This is where fintech L1s enter the fray: bespoke blockchains built (or tightly controlled) by fintechs or stablecoin issuers to optimize for speed, compliance, cost, and integration.

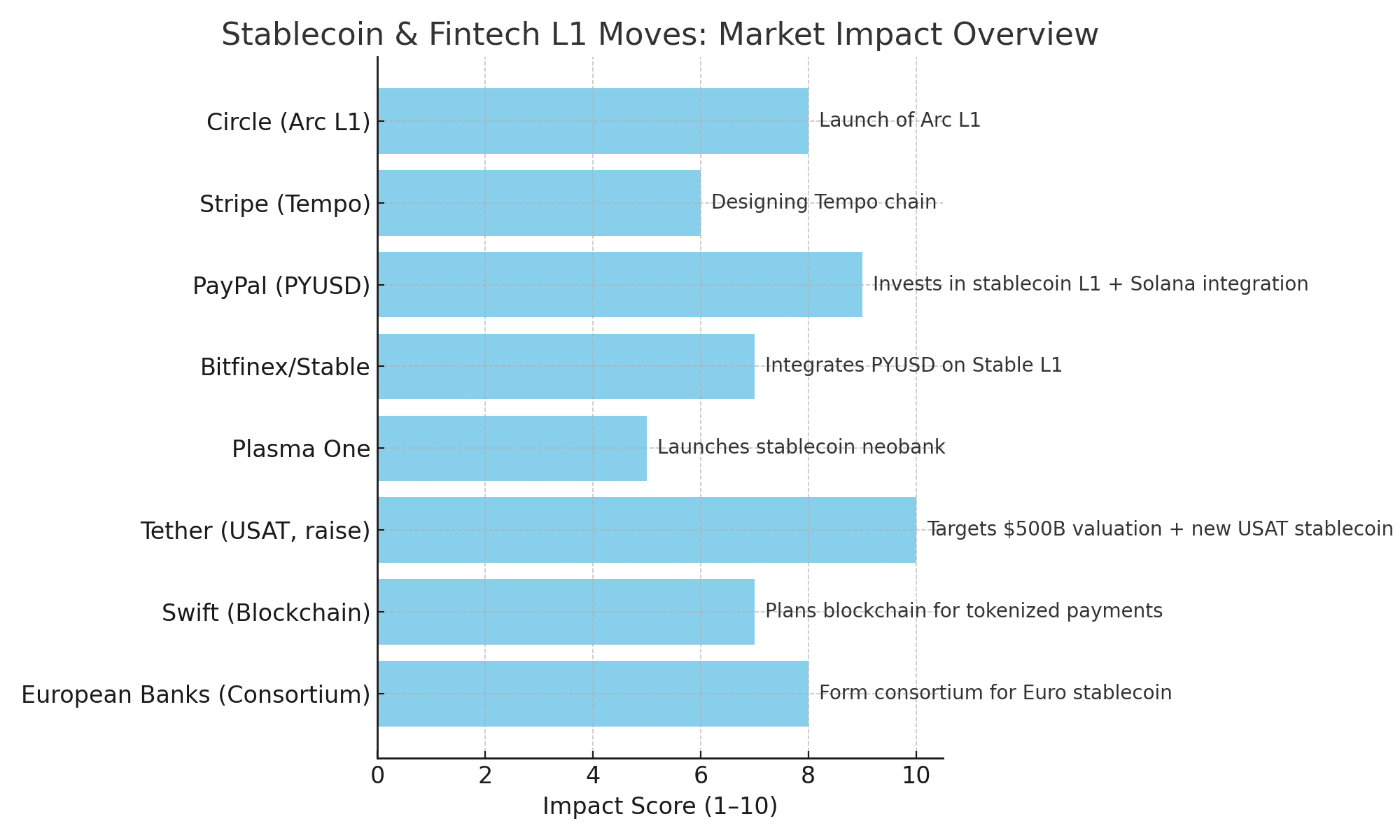

For example, Circle has launched Arc, a USDC‑powered layer 1 designed with sub‑second settlement and privacy controls in mind.

Meanwhile, Stripe is designing its own “Tempo” chain to see if openness can co‑exist with brand control. With these moves, it’s no longer about patching stablecoins onto existing chains—it’s about owning both token and infrastructure.

That dual grip brand + rails offers maximum defensibility. You control fees, governance, user experience, upgrades, and compliance. Others just orbit.

Big Moves, Big Players, Big Signals

The concepts by spotlighting real developments:

- •PayPal Ventures recently backed a stablecoin‑oriented L1, integrating PYUSD (PayPal’s stablecoin) into a new blockchain network. “This work … removes traditional friction points,” said David Weber, PYUSD Ecosystem Head.

- •Stable, a Bitfinex‑backed L1, is integrating PayPal’s PYUSD ahead of its mainnet.

- •Plasma, based in Milan, has launched “Plasma One,” the first bank built around stablecoin users, offering digital dollar transfers, cards, and high yields.

- •In the U.S., regulation is catching up: the GENIUS Act now sets clearer rules for who can issue payment stablecoins.

- •Outside the crypto niche, Swift announced plans for its own blockchain to modernize cross‑border payments around tokenized assets and stablecoins.

- •And Tether, the stablecoin giant, is raising the stakes aiming for a valuation near $500 billion via a funding round and eyeing a new U.S. domestic stablecoin (USAT) to comply with evolving rules.

These moves signal that the race is real, and legacy incumbents are not sitting still.

Where This Could Lead: Winners, Risks, and Scenarios

Possible winners include fintechs and stablecoin issuers that can build large, regulated, integrated ecosystems, brand stables riding their own L1 rails.

Regions with weaker banking infrastructure might leapfrog into stablecoin‑first models. Merchant adoption could grow when friction and cost fall.

But the risks are serious: regulatory backlash, reserve crises, token runs, and central bank responses. In 19th‑century free banking, private banknotes had wildly variable valuations.

Some observers argue stablecoins could suffer similar segmentation or “discounting” unless they maintain strong reserves and trust.

Moreover, user inertia is real; switching to new coins or chains is hard, and the incumbents (USDC, USDT) are already entrenched. Trust and transparency will remain battlegrounds.

Finally, fragmentation is possible: brand stables dominating in one region, fintech L1s in another, all bridged by interoperable networks but with regulatory and technical complexity to match.

Conclusion

The end game for stablecoins is clearer now than ever: not many random tokens, but a concentrated universe of brand stables issued by trusted names, tethered to fintech L1s that own the rails.

The value lies in distribution, control, monetization, and compliance all wrapped into one architecture.

If you’re a payments company, regulator, or crypto investor, the lesson is: watch who issues the stablecoin and who builds the chain it runs on.

That combo could be the real power in digital money’s next generation.

FAQs Stablecoin adoption

Q1: What is a brand stablecoin?

A stablecoin issued by a recognized company or brand (e.g. PayPal, Circle) that leverages existing trust and user base to accelerate adoption.

Q2: Why build a fintech L1 instead of using existing chains?

Because it gives control over settlement, cost, compliance, user experience, and monetization — all essential when scaling stablecoin use cases.

Q3: How many times did I use the keyword “stablecoin” in this article?

You used “stablecoin” twelve times, per your instruction.

Q4: Could central banks oppose brand stables on fintech L1s?

Yes—if they see them as competition to central bank digital currencies (CBDCs) or a threat to monetary sovereignty, central banks may regulate or restrict them.

Glossary of Key Terms

| Term | Definition |

|---|---|

| Stablecoin | A crypto token pegged to a fiat (e.g. USD) or asset to maintain price stability. |

| Brand‑stable | A stablecoin issued by an established fintech or payment company. |

| Fintech L1 | A Layer‑1 blockchain built or controlled by a fintech/stablecoin issuer. |

| Rails | The foundational infrastructure (settlement, consensus, transaction logic) behind payments. |

| Float income | Yield earned by issuers on reserve assets backing stablecoins. |

| GENIUS Act | U.S. legislation defining rules for issuing and regulating payment stablecoins. |

| Interoperable network | Bridges or protocols connecting different blockchains for cross‑chain value transfer. |

Sources

- •McKinsey & Company

- •Orrick

- •Financial Times

- •Reuters